Lesson M04.L01: Keynesian Economics: Core Assumptions and Historical Context

Module: Macroeconomics in the Short-Run: The Basic Keynesian Model Level: intro Duration: 30 minutes Learning Objective: Summarise the historical context of Keynesian economics (Great Depression); identify core assumptions: sticky prices, demand-driven output in the short run. Data as of: 2024 Provenance: OpenStax Macro 3e | MIT OCW 14.02

Explanation

Key Diagram

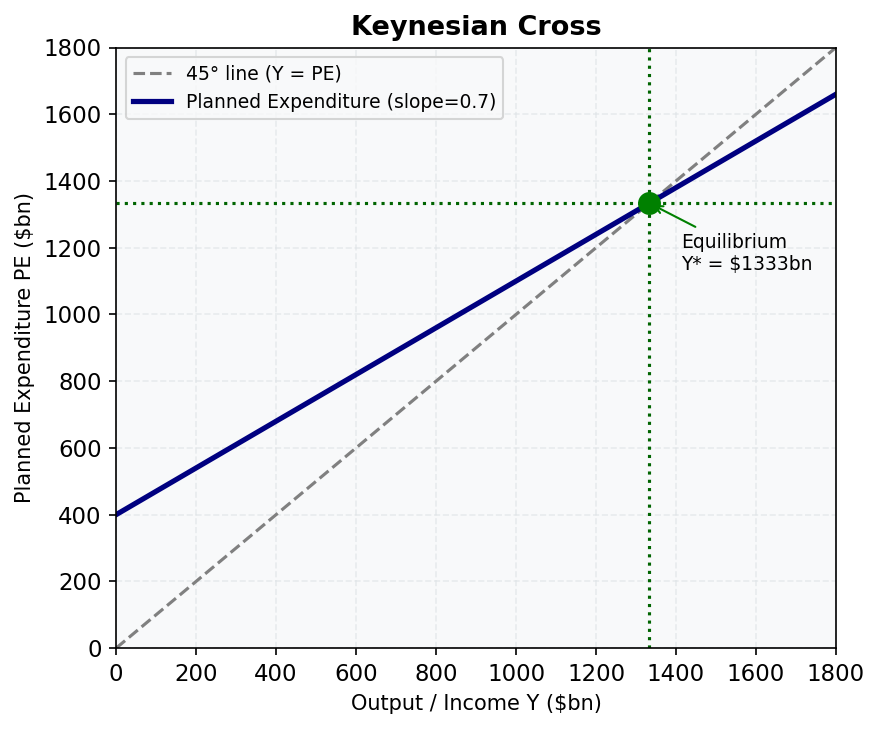

Figure 2: The Keynesian Cross. Equilibrium output Y is where planned expenditure (PE) crosses the 45° line.*

Keynesian economics is a school of macroeconomic thought developed by British economist John Maynard Keynes in the 1930s, chiefly in his 1936 work The General Theory of Employment, Interest and Money. It emerged as a direct response to the Great Depression (1929–1939), the most severe economic contraction in modern history.

The Great Depression in context: - US unemployment reached 25% by 1933; Australia's hit approximately 30% at its peak - Real GDP in the US fell roughly 30% between 1929 and 1933 - The prevailing "classical" economic view held that markets would self-correct: wages and prices would fall until equilibrium was restored. Keynes observed this was not happening — the economy was stuck.

Keynes's challenge to classical economics: Classical economists assumed prices and wages adjust flexibly and quickly, so markets always clear. Keynes argued this assumption fails in the short run:

-

Sticky prices: Prices (especially wages) do not adjust instantly downward. Workers resist wage cuts; firms fear losing customers if they cut prices. This means markets can remain out of equilibrium for extended periods.

-

Demand-driven output in the short run: Because prices don't quickly adjust, output is determined primarily by the level of spending (aggregate demand). If households, firms, and governments spend less, output falls and unemployment rises — even if prices theoretically "should" adjust.

-

Role of government: Because markets can fail to self-correct quickly, Keynes argued governments should actively manage aggregate demand — increasing spending or cutting taxes during downturns to restore full employment.

The Keynesian framework dominated economic policy in most advanced economies from the 1940s through the 1970s, and experienced a significant revival during the 2008–09 Global Financial Crisis and the 2020 COVID-19 pandemic, when Australia and other governments deployed large stimulus packages.

Worked Example

The Great Depression Mechanism (simplified):

Step 1 — Initial shock (1929): US stock market crashes. Household wealth falls sharply. Consumer confidence collapses.

Step 2 — Demand falls: Households cut spending dramatically. Firms face falling sales, so they cut production and lay off workers.

Step 3 — Classical prescription: Classical theory: wages should fall, making labour cheaper; firms rehire; equilibrium restores.

Actual outcome: Wages are sticky downward. Workers and unions resist cuts. Firms also resist price cuts fearing competitive disadvantage. The economy stays stuck at high unemployment.

Step 4 — Keynes's diagnosis: The economy is trapped in an underemployment equilibrium — a stable situation where output and employment are below full capacity. Without an external injection of spending, the market will not self-correct quickly.

Step 5 — The Keynesian solution: Government steps in as "spender of last resort." Australia's Scullin and later Curtin governments, and later the 1940s post-war reconstruction, demonstrated that public spending could restore employment. The US New Deal (1933–38) under Roosevelt was the archetypal Keynesian response.

Australia comparison: Australia's recovery from the Depression accelerated with wartime government spending in the early 1940s — real GDP grew rapidly once the government injected large spending, consistent with Keynesian predictions.

Common Misconception

Misconception: Keynesian economics argues that government spending is always better than private spending and that markets never work.

Correction: Keynes was not anti-market. His argument was specifically about the short run when prices are sticky and aggregate demand has collapsed. He explicitly acknowledged that in the long run, classical market adjustment mechanisms operate. His famous quip was: "In the long run we are all dead" — meaning that waiting for the long-run self-correction is not an acceptable policy response when people are unemployed and suffering now. Modern Keynesian models blend short-run demand management with long-run supply-side considerations.

Practice Prompts

-

Why did the Great Depression challenge classical economic theory, which predicted that recessions would be short-lived? → Answer: Classical theory assumed wages and prices would fall quickly during a recession, restoring market equilibrium and employment. In the Depression, wages and prices proved to be sticky downward — they did not fall fast enough to clear markets. Unemployment persisted at 25–30% for years, demonstrating that real economies can remain well below full employment for extended periods without automatic self-correction.

-

What are the two core assumptions that distinguish Keynesian from classical macroeconomics? → Answer: (1) Sticky prices — prices and wages do not adjust quickly in the short run, so markets do not instantly clear. (2) Demand-driven output — in the short run, the level of output and employment is determined by aggregate demand (total spending), not by supply-side factors alone.

-

How did Australia's economic policy response to the 2020 COVID recession reflect Keynesian principles? → Answer: The Australian government deployed large demand-side interventions: the JobKeeper wage subsidy (~$90 billion), enhanced JobSeeker payments, and cash grants to businesses. These were designed to support aggregate demand — keeping households spending and firms operating — consistent with Keynes's prescription of government injecting spending when private demand collapses. The policy worked: Australia's 2020 recession was short (two quarters) compared to the Depression's decade-long contraction.

Further Resources

- 📺 Fiscal Policy and Stimulus: Crash Course Economics #8 — Crash Course (12 min)

- 📺 Macroeconomics: Crash Course Economics #5 — Crash Course (12 min)

- 📚 RBA — Fiscal Policy Explainer — RBA overview of Keynesian fiscal policy principles and their application in Australia